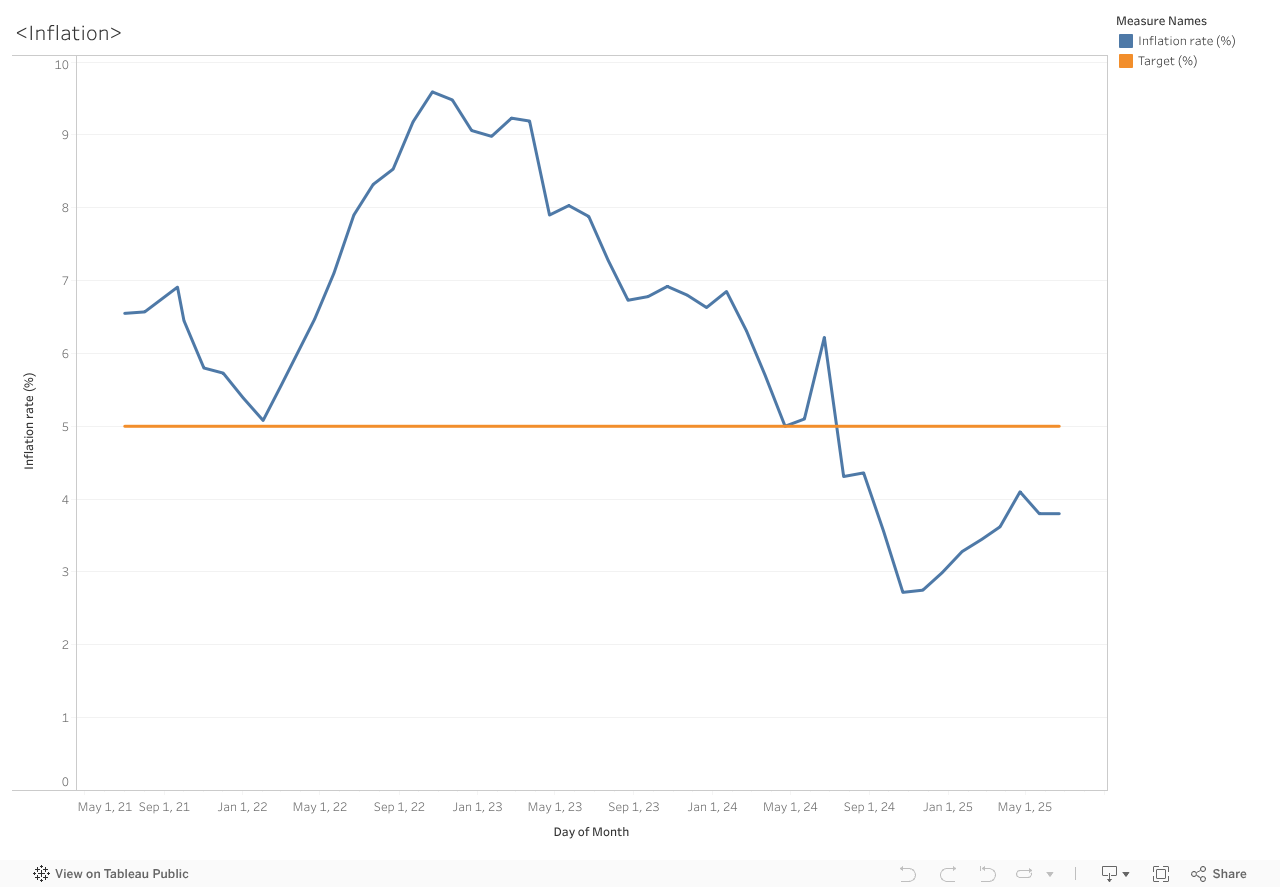

Kenya’s inflation was 4.1 % in April 2025—up from roughly 3.6 % in March 2025

Since early 2021, Kenya’s inflation rate has risen and fallen around the Central Bank’s 5 percent target line. It sat a little above that goal through much of 2022, then surged to almost 10 percent in January 2023 when global fuel and food prices spiked.

Tight monetary policy, better harvests, and cheaper imports helped pull inflation back to about 5 percent by mid-2024 and down to roughly 3 percent in January 2025. Since then, prices have ticked up again, reaching just over 4 percent in April 2025—still under the target but on the rise. The 5 percent target matters because it guides expectations: if inflation climbs far above it, the Central Bank signals it will act (for example, by raising interest rates) to keep people’s purchasing power from eroding; if inflation falls well below it, the Bank can ease policy to support jobs and growth.

In short, the target acts like a steady line on a roller-coaster chart, helping households and businesses plan while policymakers work to keep price growth neither too hot nor too cold.

Core and Non Core Inflation

Kenya’s core inflation was 2.5 % in April 2025, higher than March’s 2.2 %, while non-core inflation climbed to 8.4 % from 7.4 %.

Over the past ten months, Kenya’s price story has really been two different tales. The “core” part of inflation—which strips out volatile items like fuel and fresh produce—barely moved, hovering in a narrow band of roughly 2 percent. After dipping to about 1.8 percent in October 2024, it inched back up and stood 2.5 percent by April 2025. This steadiness tells us that underlying, longer-term price pressures have remained tame.

The “non-core” side, however, was far more dramatic. It started at about 11 percent in July 2024, plunged through the second half of the year (as global fuel costs eased and harvests improved), bottomed out near 4 percent in October, and then climbed again—landing 8.4 percent this April after fresh jumps in energy. In other words, the volatile categories that households feel most immediately at the pump and the market have been on a roller-coaster, while everyday essentials such as rent, school fees, and packaged foods have risen only slowly.

Taken together, the chart shows that Kenya’s recent inflation bump is being driven mainly by swings in fuel and fresh food, not by broad-based price creep. As long as core inflation stays low, the central bank has some breathing room; its bigger challenge is cushioning consumers against those sharp, often unpredictable spikes in non-core costs.